Which structure is right for you?

So you’ve heard that VC firms won’t invest in you unless your business is a C corporation. There is some truth to this. Many venture firms may require you to be a C corp at some point, with some states being more favorable for incorporation than others (Delaware is a popular one). Some reasons could be to minimize admin work related to a partnership return, gain exclusions, predictable taxation, and/or limitations of Limited Partners (LPs) within a fund with a specific business structure.

Ultimately, investors wouldn’t pass up investing in an amazing founder solely due to the business structure (like an LLC). Conversely, your business will not be more valuable simply because you started out as a C corp; so structure businesses for needs and not prestige.

Formation

A business can form a Sole proprietorship, Partnership, (LP, LLP), LLC, and Corporation. Some businesses have heavier reporting requirements than others. Corporations generally have more financial and reporting requirements than LLCs, partnerships, and sole proprietorships. The requirements may vary state to state. In general, a business organizes, or files articles. Businesses adhere to local and federal law in addition to any operating agreement agreed upon by owners.

Business structure ties into legal and personal risk, so for that reason I generally will not recommend setting up your business as a sole proprietorship or a partnership that isn’t limited for the long term. The owner is held personally liable, as are their assets. Hence there’s not much in the way of protection for business owners. Note: Not formally structuring a business defaults you to being a sole proprietorship. A limited Partnership, LLC, Corporation, and S corp generally have some form of limited liability, some are considered separate entities. This separation is valuable for owners as it provides a level of legal and financial protection.

Consider taxation

An LLC is a business entity, but may be taxed as if it is a Sole proprietorship, Partnership, Corporation, or S Corp. How it is taxed generally relates to how many members there are or elections made (you have to elect to be taxed as a C corp or S corp). Partnerships, Sole Proprietorships, and S Corps are pass-through entities. Pass-through means that losses and gains are “passed” onto the members personal tax return, and the entity itself doesn’t pay corporate taxes. C Corporations see double taxation, meaning that a C Corp will pay a Corporate tax on its profits, and then shareholders will pay tax again on any dividends.

Self-employment tax (SE tax)

As an LLC taxed as a sole proprietorship, partnership, or S corp, you’d be responsible for SE tax of 15.3%. This cost is typically split with employees. When you’re an owner-employee you pay both sides of the tax, in addition to any pass-through profits (partnerships and sole proprietorships). Corporations of course have to pay employment taxes, but the employment tax doesn’t apply to the profits themselves. Similarly this concept is what makes the S corp election appealing to some businesses as they begin to have significant profits year to year. Although an S corp is a pass-through entity, the SE tax is limited to what is paid to the owner, and not the profits themselves. Note: There are rules surrounding who can elect to be an S corp, and possible salary requirements for owner-employees of these businesses.

Below are some differences to consider when thinking of these entities:

Pass-through entity

Above we mentioned which structures typically will have pass-through activity. Below we explore who will inherit the year-end business activity depending on structure. Losses will typically pass through to owners in a partnership, sole-proprietorship, and S corp. Remember an LLC can be taxed as a partnership, sole-proprietorship, S corp, etc.

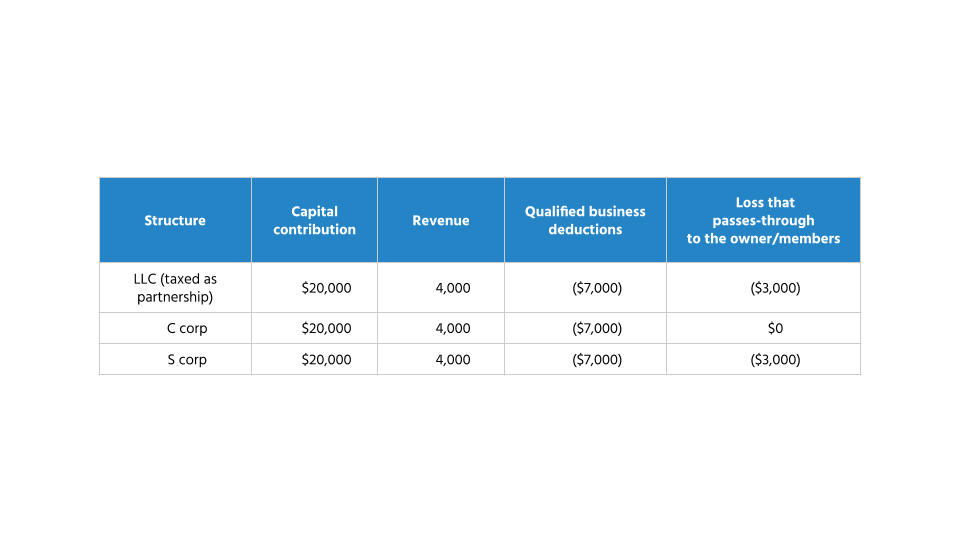

Note: To expound on tax effects, a founder should discuss with a tax practitioner to best understand how these choices will affect their overall tax liability. The tax effect of a business loss or gain can be complicated, and is not uniform for every tax payer. There may be times where an owner can’t utilize a loss due to a lack of tax basis, waterfalls, loss limits, etc. How these may affect you are worth considering when forming a business. Below you will see a few examples that are meant to get you thinking about the possibilities of what could happen within a structure, but may not apply exactly as shown below.

The below tables are meant only to display pass-through activity visually.

In the example below, let’s consider a business that is newly founded and operated full-time by two individuals. They have a tax basis in the business and no other significant outside financial activity.

Using the same information as above, let’s see what is passed through when the business generates a positive net income. (Note: determinations of how income is distributed may depend on legal structure, capital contributed, operating agreements etc.)

So what is right for you?

Reflecting on what matters most for yourself, you can create a decision graph for yourself to help decide. Below is an example of that.

In short, start a business that best fits your business needs. Early on an LLC may be favorable to some due to ease of setup and cost. Corporations may be helpful for preparing to go public or the needs of an entity completely separate from the individual.

There may come a time when it is necessary for you to convert due to new owners and their requirements. Luckily, business structures can be changed, so a founder may choose to start as an LLC, and later convert the business into a C corp when one structure suits their needs over the other. Or a founder may decide to avoid having to convert later, and simply start with a C corp. Whichever you choose, remember to ask questions that are relevant to your problem. What are the short and long-term goals for the business? Based on the industry is there a benefit to forming a certain type of entity? What kind of exposure am I willing to accept? How does my state treat this type of structure? There are many more questions you could ask yourself, but most importantly get started. Choose something that maximizes your benefit throughout your entrepreneurial journey.